In last year's Budget, the government changed Malta's personal income tax. Between 1995 and 2017, the share of personal taxes in total tax revenue ranged between 16.5% and 20.3%. It then continued rising steadily to 27.0% by 2023. The 2025 budget introduced changes to the income tax brackets ̶ increasing the tax-free income thresholds by €2,900 for singles, €2,300 for married couples, and €2,500 for parents ̶ as well as raised the lower bounds of the 15% and 25% tax brackets.

According to economic theory, tax cuts increase household demand by increasing workers' take-home pay. Some tax cuts can boost business demand by reducing the cost of capital, thereby making investment spending more attractive. Business tax cuts also increase firms' after-tax cash flow, which can be used to pay dividends and expand activity. But here we are talking about personal taxation, not corporate taxes.

When demand from households and businesses rises, firms producing goods or offering services increase production and hiring to meet the demand, thereby expanding output and reducing unemployment. This "economic growth" can lead to an increase in the annual GDP growth rate, a one-time increase in the size of the economy that does not affect the future growth rate but puts the economy on a higher growth path, or both.

This focus on the supply side of the economy in the long run is in contrast to the short-term phenomenon, also called "economic growth", by which a boost in aggregate demand, in a slack economy, can raise GDP and help align actual GDP with potential GDP. At times when the economy is already near its potential level of output ̶ which is Malta's case ̶ or when supply is constrained in other ways, policies that increase demand can boost inflation. More on this later.

Tax reductions can be expected to encourage individuals to work, save, and invest, though they also have certain downside risks. The net impact of tax reductions on growth is uncertain, but many estimates suggest it is either small or negative. The effect of tax cuts on budget deficits can be offset by broadening the tax base, usually by eliminating exemptions, exclusions, deductions, credits, and other preferences. However, base-broadening may reduce the impact on labour supply, saving, and investment, thus reducing the direct impact on growth. It may also reallocate resources across sectors toward their highest-value economic use, resulting in increased efficiency and potentially raising the overall size of the economy.

Results in the literature suggest that not all tax changes will have the same impact on growth. Reforms that improve incentives, reduce existing distortionary subsidies, avoid windfall gains, and avoid deficit financing will have more auspicious effects on the long-term size of the economy, but may also create trade-offs between equity and efficiency.

The government eschewed any tax-base broadening measures. That meant that the full positive effects of tax reductions would be felt by households. On the other hand, it also meant that the negative effects on the fiscal deficit could not be avoided. Another possible restraint on the negative effects - interest rate rises - was clearly not possible once we lost control of monetary policy to the European Central Bank.

So, what can we expect from the changes announced last year? This is explored in a recent paper by Glenn Abela and Ian Debattista, two senior economists at the Central Bank of Malta. They examined the economic impact of these changes on households, public finances, and the broader economy. Results were derived through simulations carried out in EUROMOD (a tax-benefit micro-simulation model for EU countries) and MEDSEA (a small open economy DSGE model of the Maltese economy).

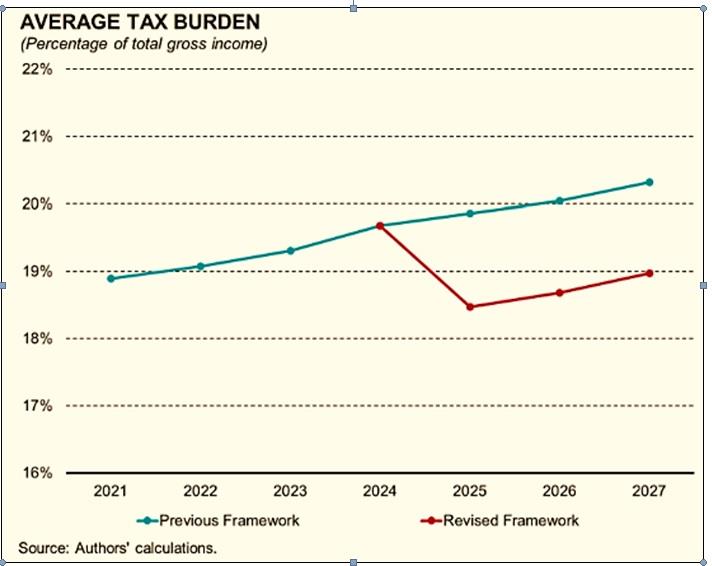

The authors estimated that the tax liability of the average taxpayer in 2025 would fall by €595 as a result of these adjustments. The average household will see its annual disposable income increase by €703 (or 1.7%). The figure increases to €988 (2.0%) for households that are directly affected. Middle-income households are expected to gain the most in relative terms. The average tax burden (see chart) is expected to decline by 1.4 percentage points, reversing the recent upward trend attributable to fiscal drag (the additional proportion of income tax received by the Inland Revenue as income rises). Similarly, middle-income households are the most affected.

Government revenue from personal income tax in 2025 is expected to decrease by 9.8% or €168 million (equivalent to 0.7% of GDP), compared to what would have happened had no changes been made in the tax framework. The results have an impact on the so-called 'tax-to-base elasticity', which essentially measures how much the tax base changes when the tax rate is adjusted (either increased or decreased). Elasticity is estimated to increase from 1.61 under the previous tax framework to 1.73, indicating a more responsive framework to increases in income levels.

The revised brackets also enhance the redistributive role of the tax system by reducing income inequality. They do this through both larger decreases in the Gini Coefficient and a higher Kakwani Index (a measure of the progressivity of a social intervention used by social scientists and economists). Additionally, although more targeted towards middle-income households, this reform helps to alleviate poverty, as the share of households below the pre-reform poverty line decreases by 0.23 percentage points.

The broader impact of the reforms is assessed through MEDSEA. Here, a model is used to determine the effect of a permanent reduction in the effective labour tax rate in Malta. This shock leads to an increase in net real wages, boosting household consumption, especially among 'hand-to-mouth' households. In the short term, the increase in consumption ̶ and thus economic activity ̶ leads to even higher wages and increases in domestic prices, resulting in reduced export competitiveness.

However, the tax reduction also incentivises employment, leading to an increase in the number of hours worked. This subsequently lowers real gross wages, thereby reducing domestic price pressures and increasing export competitiveness over the medium term. The authors do not dwell on this sufficiently, though. If the increase in hours worked is due, say, to higher female labour force participation or to more overtime by Maltese nationals is one thing; if it happens through more foreign nationals coming to Malta is another.

How much the tax cuts boost demand depends on the sensitivity of household and business behaviour. In other words, it all turns on how households will divide increased after-tax income between consumption and saving, and whether businesses choose to hire and invest more. Economists summarise these effects in a simple measure, the output multiplier, showing how many euros of increased economic activity result from a one-euro reduction in taxes.

The stimulus from tax cuts depends on the strength of the economy. If it is operating close to potential, fiscal policies will have a smaller short-run economic effect. Most economists estimate that fiscal multipliers are about three times larger when the economy is very weak, than when it is strong. Given that the Maltese economy is operating at close to its potential, real GDP is expected to increase, albeit modestly. The authors of the CBM study expect this will be the case, especially in the outer years of the simulation horizon, reaching a peak of around 0.4% above the no-reform baseline level.

Both the Prime Minister and the Minister of Finance failed to tout the economic growth aspect of the tax cuts, preferring instead to concentrate on the impact on middle-class taxpayers. Perhaps, in future the Finance Minister should pay more attention to base-broadening tax reforms, which have the additional benefit of reallocating resources from sectors that are currently tax-preferred to sectors that have the highest economic (pre-tax) return.

Frans Camilleri is an economist. He studied at Oxford and University of East Anglia, is a former corporate head at Air Malta, and has served on various public and private boards.