Not a week passes by that we don't read reports that some country's indigenous population is at risk of disappearing because of collapsing fertility. Demographic doom has become pervasive: as declining birth rates cause populations to shrink, longer lifespans will lead to ballooning costs of pensions and healthcare. A shrinking workforce will have to pay for it all.

Malta's indigenous population is projected to decline too. The latest projection shows a 14% drop in native Maltese by 2050. However, the total population is expected to grow through migration. Malta is one of 11 EU countries that will have population growth by 2100, all the others being in negative territory.

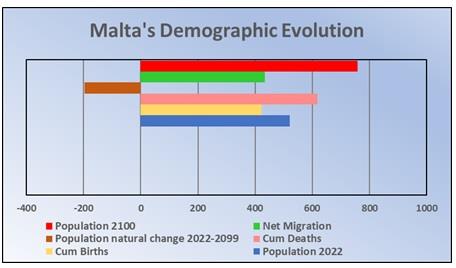

The demographic changes are shown in the chart (below). The natural change in the population will be a negative 196,000 as deaths will exceed births. But the net migration of 238,100 people will compensate for the negative natural change and take the population up to 759,100 by 2100. Only a striking rise in the fertility rate could mitigate the need for foreign migrants.

The demographic dividend that has supported global economic expansion in recent decades has turned into a demographic drag. In developed countries, the share of working-age people is shrinking. In Malta, it will fall from 63.2% in 2022 to 51.5% by 2070. Falling fertility and rising longevity have significant implications for the trajectory of the world economy.

A recent study by the IMF's Research Department weighs the economic headwinds from older populations against the tailwinds from healthy aging. It shows that, thanks to better health, improved labour market outcomes for people aged 50 and over could add 0.4 percentage points annually to global GDP growth in 2025-50. Failing action by governments, global growth would be about one percentage point slower than in pre-Covid years. Demographic drag would account for almost three-fourths of the decline. On the other hand, if governments were to implement policies that improve people's human capital and keep them in work as they age, this could offset a lot of the growth drag.

The pessimism around an ageing population is overdone. According to the OECD, nine out of every ten workers added to the labour force in Europe in the past decade, came from a jump in workers over 50. Therefore, there is no reason why economic dynamism should suffer if more older people continue working. If the approach to ageing is reframed, societies can reap a "longevity dividend".

For too long, the policy debate has focused on changes in the state retirement age. Australia, Denmark, and Belgium have done it in recent years; the UK is next. Between 2012 and 2023, the average age at retirement in the EU increased, rising from 59.2 years to 61.3 years, a gain of 2.1 years. This upward trend reflects a shift towards later retirement in many EU countries. Malta's last change was in 2006, when it was decided to raise the retirement age to 65 years by 2027.

In many countries, raising the state retirement age has generated widespread resistance; the troubles in France were perhaps the most conspicuous. Now, it seems that many countries are chasing the fertility rate chimera, even though policies aimed at raising birth rates are expensive and have had relatively modest effects, given that they fly in the face of personal preferences. A third solution ̶ immigration ̶ holds political challenges. Don't we know that in Malta!

The problem is that the latter two policies aim at changing the relative size of different age groups but do not address the deeper challenge of how society adjusts to longer lives. If longevity is what makes our pensions and health systems unsustainable, higher birth rates or immigration merely delay the financial day of reckoning.

Therefore, while raising the retirement age helps public finances, this should be accompanied by measures that assist individuals to work longer. A broader policy spectrum would include a range of policies across all ages. The main areas of focus are health, skills, and the creation of age-friendly jobs.

With an ageing population, health is important not just for individual welfare but also for the entire economy. Preventive health policies yield a substantial macroeconomic value. Some experts in the UK have calculated that a 20 percent reduction in the incidence of six major chronic diseases increases GDP by one percentage point within five years and 1.5 p.p. in ten years, thanks to higher labour force participation. The effect is most pronounced for workers ages 50 to 64.

However, good health alone is not enough to keep people in employment longer. Older people tend to prefer age-friendly jobs, such as those with more flexible hours, fewer physical demands, and greater autonomy. Because certain occupations remain problematic for older workers, policies need to be developed to help them reskill and transition into new occupations throughout life.

One major challenge is to stop seeing an ageing society as a problem. It is rather ironic that what is one of the greatest achievements of the 20th century, namely that people are living longer and healthier lives, is often viewed in a strikingly negative way. Instead, it is an opportunity.

The second challenge is to abandon the unworkable focus on changing individual behaviour. Instead of trying to preserve current systems, we should focus on helping older and more experienced persons adapt to greater life expectancy. This involves a new approach to ageing based on redesigning health systems and investing more in our later-life human capital.

A longer life causes a profound change in outlook. Previously, when the chance of living long enough to become old was slim, investing to benefit a future octogenarian made little sense. But now that global life expectancy is exceeding 70, or even 80 years, in an increasing number of countries, it does. Logically, this has radical implications for our health, education, work, and financial systems. Traditional approaches will no longer work.

For example, the health burden in many countries is shifting from infectious to chronic non-communicable diseases, the latter now accounting for 60 percent of the disease burden globally, and 81 percent in the European Union (Malta: 82%). This explains why healthy life expectancy has not grown as fast as overall life expectancy, causing an expansion of morbidity.

The current health system is at risk of keeping us alive but not healthier for longer, at an ever-increasing cost to individuals, families, and society. In 2022, health expenditure in Malta was 9.5% of GDP, compared to an average 10.4% in the EU. That was well below Denmark's 12.6% but almost double Romania's. That may be expected to rise considerably; suffice to say that expenditure on long-term care is projected by the European Commission to rise from 1.0% of Malta's GDP in 2020 to between 2.3%-4.2% in 2070.

Instead of adding years to life, we must add life to these extra years. What we need is a shift toward chronic disease prevention and health maintenance, using genetic data for targeted medical interventions, utilising advances in biology to postpone the incidence of multiple diseases, taxing unhealthy food, improving cognitive capacities, and exploiting the better health potential by reducing poverty.

Some researchers have conducted simulations showing that health policies could boost global annual output growth by about 0.6 p.p. over 25 years, offsetting almost three-fourths of the estimated demographic drag during that period. Such a gain would mitigate rising health and social care costs.