Skyrocketing house prices and rents in Europe risk making housing unaffordable in many countries. There is alarm about the broader implications of the housing crisis, such that Eurofound has warned of homelessness, housing insecurity, and financial strain. These problems undoubtedly impinge on people's health and well-being, generate unequal living conditions and opportunities, and result in higher healthcare costs, reduced productivity and environmental damage.

It is a tragedy that housing has become a commodity treated as an investment vehicle by the ultra-wealthy and a lucrative short-term tourist rental for owners. It is an increasingly unattainable dream for many. Rampant financial speculation has transformed the residential property market into one where profit is prioritised over human need.

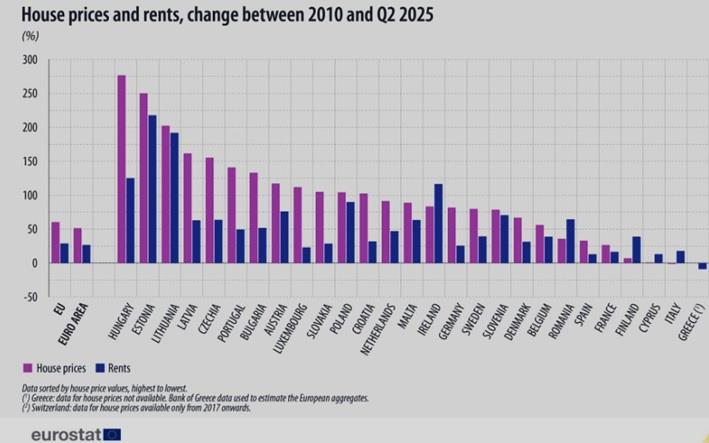

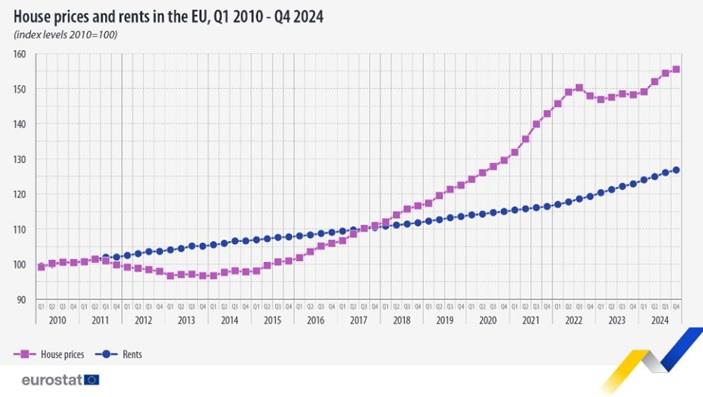

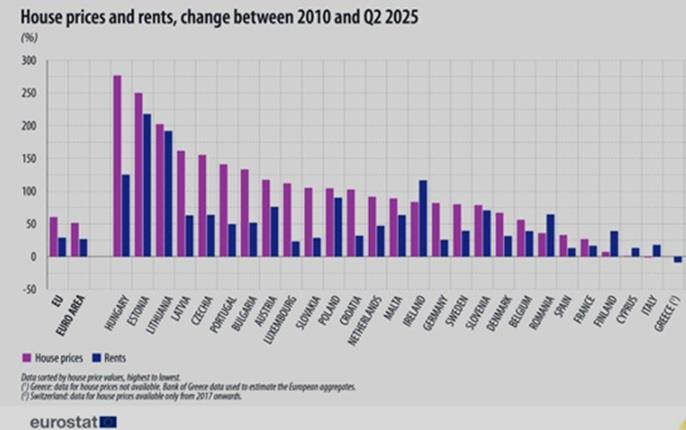

The latest figures from Eurostat show that house prices in the EU increased by some 62 percent (Malta: 89 percent) over 15 years, while EU rents rose by 26 percent (Malta: 62 percent). The house prices/rent ratio in the EU has widened by a fifth over the period. One in ten Europeans now spends 40% or more of their disposable income on housing (Malta:12%).

Today's youths confront a bitter paradox: their access to affordable housing is lower than that of their grandparents and parents who lived in the materially poorer decades following World War II. Today's far wealthier societies seem incapable of providing decent, affordable homes for ordinary people. One statistic provides a stark indicator of this crisis: one in five Europeans aged 30 to 34 lives with parents.

We boast about the success of financial services in Malta. Now, we want to attract high-value-added industries, particularly in AI, to Malta. But has anybody asked what this is going to do to home prices and rents? For this to happen, we will need to attract highly skilled professionals, particularly in areas such as technology and informatics. These are the kind of people who will command above-average salaries, and they will surely outbid the average Maltese, in the process pushing prices further up.

Why have most governments largely abandoned housing provision to unchecked market forces? In my view, this has nothing to do with economic capacity but is due to the lack of political will. The consequences of this policy failure are profoundly political, socially corrosive, and demonstrably destabilising to the fabric of democratic societies.

The housing shortage feeds a pervasive sense of insecurity, disenfranchisement, and abandonment among significant segments of the population. Job precariousness, relatively stagnant wages, the erosion of essential public services, and housing insecurity create fertile ground for xenophobic movements that cunningly exploit legitimate grievances. The far right weaponises the housing crisis by advocating homes and resources for "own citizens" while explicitly excluding immigrants, minorities or other perceived outsiders.

The share of social housing in total supply in the EU has been shrinking since 2010, even though the number of vulnerable people, such as the homeless or new migrants, has risen. In Malta, it is one of the lowest, with a share of 5.1%, compared to 32% in the Netherlands. Moreover, half of Europe's housing stock was built before 1980, and many buildings are energy inefficient. Bringing those homes and apartments up to new EU standards will be expensive and take a long time.

Dan Jørgensen, the EU Commissioner for Energy and Housing, recently told a conference that the housing crisis "threatens social justice and social cohesion ... It weakens our economy and reduces our competitiveness." Chiara Fratto, a European Investment Bank economist who researches housing issues, adds that "we need to enhance the housing supply while also making better use of the stock we already have."

It is obvious that housing demand is outstripping supply while incomes aren't keeping up with prices. To close the supply gap, we need to adopt faster and less costly ways of building, assist the construction sector in adopting innovative technologies and materials (robotics, improved energy efficiency, and emission cuts), and enhance the investment framework for housing cooperatives to deliver affordable new apartments and homes. Also, since urban land is in short supply, high-rise housing should be promoted while smaller families and childless families should be encouraged to live in smaller homes.

For existing homeowners, rising house prices have been a windfall. Fratto, who co-authored the EIB Investment Report section on housing, says that this wealth creation has benefitted low-income homeowners as well, particularly since housing tends to make up a large share of their assets. "Homeowners benefited a lot from the increase in house prices because they saw huge increases in their wealth," she says.

Meanwhile, those with second homes in tourist hotspots have also seen gains from rising values and strong rental demand. "For some people, like those providing accommodation, having a second home that you can rent has been a huge benefit," she says.

A study in the United States found that improving the availability of housing in key cities could have raised aggregate gross domestic product by up to 9%. Fratto is trying to replicate the same sort of analysis for European housing markets.

Housing shortages have long-term effects. People who found themselves homeless at one point have less chance of being employed in the future. Over 13 million people in the European Union experienced housing difficulties in the past five years. Those people were more likely to be unemployed - 15% vs. 8% in the rest of the population - even when the reason for being homeless was not financial.

Social and affordable housing needs more money and a better regulatory framework. New financing models could be used to attract investment, but they need to be paired with public policies that aid the development of social and affordable housing. Many countries lack the legal and policy framework that would encourage the creation of affordable housing providers, although they are trying to develop these frameworks based on guidance provided by other EU countries. Finding new ways to blend grant funding with commercial funding will also help leverage private capital.

The European Investment Bank has financed nearly a half a million social housing units across 16 countries since 2018 - including the Irish housing association that built Anselm Leahy's new apartment. But we, and everybody else, need to do more. The housing crisis is increasing inequality and limiting opportunities for an entire generation of young people. "It creates all these intergenerational issues," Sinnott says. "You have problems providing basic public services. You block people out of a source of wealth. You prevent needed migration."

"The housing crisis," she says, "fundamentally puts Europe's economic and social model under strain."

The EIB's housing plan

To tackle some of these issues, the EIB Group is introducing an action plan for affordable and sustainable housing. Under the plan, we aim to increase lending for housing to €4.3 billion in 2025. That money, along with advisory support, will be used to support three key areas: innovation, renovation and new building. The plan aims to:

- Increase financing and advisory support for innovative new construction methods and materials, through funds dedicated to support innovative construction methods and materials manufacturing;

- Push to extend lending across all EU members, while also sharing advice on building or improving the policy and regulatory frameworks that underpin investment;

- Expand the scale and reach of energy efficiency projects, especially building renovation, which will be complemented by advisory support for energy efficiency programmes and financial instruments;

- Expand investment across the publicly regulated affordable housing sector, with a focus on rental properties and pilot programmes that would help people eventually own their dwelling, depending on local regulations and safeguards;

- Test and scale up financing approaches, such as a new financial instrument for blending EU grant financing with loan financing from the EIB or other lenders.

The EIB has been financing housing for over 25 years. Tanguy Desrousseaux, director of the EIB's Housing, Cities and Regions Department, points out that the plan will add momentum to lending and advisory activities, and allow for tried and tested solutions to be scaled up and new approaches to be developed with partners.

"Delivering affordable and energy efficient housing - and using innovative construction technologies to bring down costs - is a key challenge across the whole European Union. The EIB has a unique opportunity to intervene across the housing value chain."

The Affordable Homes Initiative is making hundreds of homes available for less. Way less. Around 30% below comparable market prices. These homes will be available for working individuals and couples with or without children who are on lower to middle income and have limited assets. We are doing this by collaborating with private builders who will deliver modern quality homes that are environmentally sustainable at a lower price. Homebuyers will benefit from a quality home, and a certain affordable pathway to homeownership. The Foundatioin for Affordable Houising, will be offering 260 affordable homes made possible through collaboration between Church and Government.

The Housing Authority offers 12 schemes that contribute towards making housing more affordable. Some of these schemes are direct government initiatives, whereas others involve collaboration between the government and landlords, tenants, and the banks. The targeted groups include first-time buyers, people on social assistance, pensioners, low-income earners, owners of vacant properties. The tools being used include rent subsidies, tax incentives, loan guarantees, waiving of certain property fees, and outright grants to purchase a property.

Malita Investments has been addressing this critical issue since 2016. The quasi-public institution plans to deliver 752 apartments, and 698 parking spaces and garages by 2026.